|

|

| Line 5: |

Line 5: |

|

| |

|

| Note also the interrelationship between [[CEUM]] and the {{isdaprov|Ratings Downgrade}} {{isdaprov|ATE}}. One can be forgiven for feeling a little ambivalent about {{isdaprov|CEUM}} because it is either caught by {{isdaprov|Ratings Downgrade}} or, where there is no requirement for a general Ratings Downgrade, insisting on {{isdaprov|CEUM}} seems a bit arbitrary (i.e. why do we care about a downgrade as a result of a merger, but not any other downgrade?) | | Note also the interrelationship between [[CEUM]] and the {{isdaprov|Ratings Downgrade}} {{isdaprov|ATE}}. One can be forgiven for feeling a little ambivalent about {{isdaprov|CEUM}} because it is either caught by {{isdaprov|Ratings Downgrade}} or, where there is no requirement for a general Ratings Downgrade, insisting on {{isdaprov|CEUM}} seems a bit arbitrary (i.e. why do we care about a downgrade as a result of a merger, but not any other downgrade?) |

| | ===1992 upgrade=== |

| | Even before the {{2002ma}} was published it was common to upgrade the {{1992ma}} formulation to something resembling the glorious concoction that became Section 5(b)(v) of the {{2002ma}}. The 1992 wording is a bit lame, really. |

| | |

| | Here’s a snapshot of the difference: |

| | |

| | |

| | [[File:CEUM delta.png|450px|thumb|center|What what once was, overlaid with what now is.]] |

Revision as of 11:20, 14 November 2017

|

2002 ISDA

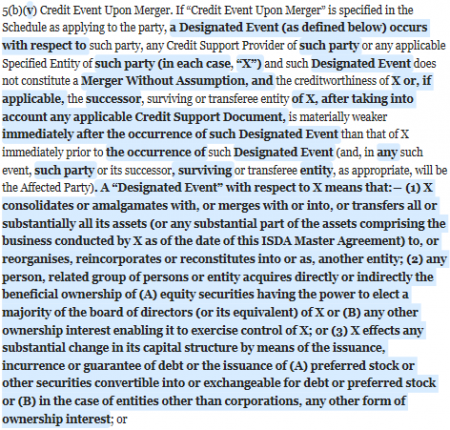

- 5(b)(v) Credit Event Upon Merger. If “Credit Event Upon Merger” is specified in the Schedule as applying to the party, a Designated Event (as defined below) occurs with respect to such party, any Credit Support Provider of such party or any applicable Specified Entity of such party (in each case, “X”) and such Designated Event does not constitute a Merger Without Assumption, and the creditworthiness of X or, if applicable, the successor, surviving or transferee entity of X, after taking into account any applicable Credit Support Document, is materially weaker immediately after the occurrence of such Designated Event than that of X immediately prior to the occurrence of such Designated Event (and, in any such event, such party or its successor, surviving or transferee entity, as appropriate, will be the Affected Party).

- A “Designated Event” with respect to X means that:―

- (1) X consolidates or amalgamates with, or merges with or into, or transfers all or substantially all its assets (or any substantial part of the assets comprising the business conducted by X as of the date of this ISDA Master Agreement) to, or reorganises, reincorporates or reconstitutes into or as, another entity;

- (2) any person, related group of persons or entity acquires directly or indirectly the beneficial ownership of (A) equity securities having the power to elect a majority of the board of directors (or its equivalent) of X or (B) any other ownership interest enabling it to exercise control of X; or

- (3) X effects any substantial change in its capital structure by means of the issuance, incurrence or guarantee of debt or the issuance of (A) preferred stock or other securities convertible into or exchangeable for debt or preferred stock or (B) in the case of entities other than corporations, any other form of ownership interest; or

(view template)

1992 ISDA

- 5(b)(iv) Credit Event Upon Merger. If “Credit Event Upon Merger” is specified in the Schedule as applying to the party, such party (“X”), any Credit Support Provider of X or any applicable Specified Entity of X consolidates or amalgamates with, or merges with or into, or transfers all or substantially all its assets to, another entity and such action does not constitute an event described in Section 5(a)(viii) but the creditworthiness of the resulting, surviving or transferee entity is materially weaker than that of X, such Credit Support Provider or such Specified Entity, as the case may be, immediately prior to such action (and, in such event, X or its successor or transferee, as appropriate, will be the Affected Party); or

(view template)

Index: Click ᐅ to expand:Navigation

|

|

- Section 5(a)(viii) is Merger Without Assumption.

Pay attention to the interplay between this section and Section 7(a) of the Transfer Section. You should not need to amend Section 7(a) (for example to require equivalence of credit quality of any transferee entity etc because that is managed by CEUM.

Note also the interrelationship between CEUM and the Ratings Downgrade ATE. One can be forgiven for feeling a little ambivalent about CEUM because it is either caught by Ratings Downgrade or, where there is no requirement for a general Ratings Downgrade, insisting on CEUM seems a bit arbitrary (i.e. why do we care about a downgrade as a result of a merger, but not any other downgrade?)

1992 upgrade

Even before the 2002 ISDA was published it was common to upgrade the 1992 ISDA formulation to something resembling the glorious concoction that became Section 5(b)(v) of the 2002 ISDA. The 1992 wording is a bit lame, really.

Here’s a snapshot of the difference:

What what once was, overlaid with what now is.